Fintech

Quick Answer

Fintech is no longer just about digitizing banking; it’s about Embedded Finance and Open Data ecosystems. Success in this space requires a dual mastery of high-growth technology and the rigorous regulatory requirements of authorities like the BSP and SEC.

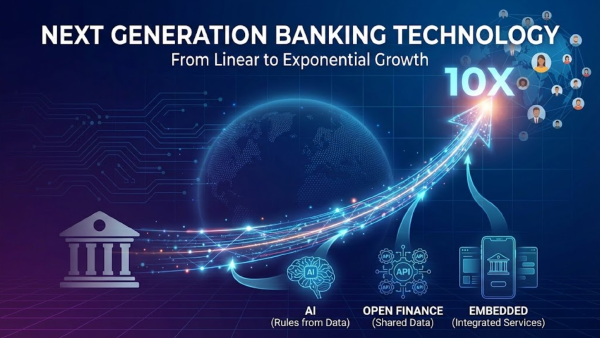

Open & Embedded Finance: The New Plumbing#

The future of financial services isn’t found in a banking app; it’s found inside the apps where people already live. Embedded Finance is the integration of financial services into non-financial platforms—think insurance at the point of sale or credit within a supply chain app.

Open Finance is the underlying plumbing that makes this possible. By unlocking data through secure APIs, we move from a world of “Bank-led” finance to “Customer-led” finance. For the executive, this represents a massive shift in how value is captured and distributed.

Regulation as a Strategic Moat#

In emerging markets like Southeast Asia, regulation is often seen as a hurdle. In reality, mastery of the BSP (Bangko Sentral ng Pilipinas) or SEC frameworks is a powerful strategic moat.

Navigating the Basel frameworks, AMLA requirements, and digital banking licenses isn’t just a compliance task; it’s an architectural one. If you build your tech stack with “Regulation by Design,” you can scale faster and with less risk than competitors who treat compliance as an afterthought.

Scaling the Fintech Stack#

Scaling a fintech is fundamentally different from scaling a SaaS platform. You aren’t just moving bits; you are moving value, and that requires a level of resilience, security, and auditability that is non-negotiable.

We focus on the “Fintech Infrastructure” that allows for:

- High-throughput ledgers: Handling millions of transactions with zero-drift.

- API-first modularity: Allowing for easy integration with ecosystem partners.

- Real-time Risk Management: Using AI and data to mitigate fraud and credit risk at the point of transaction.

Frequently Asked Questions

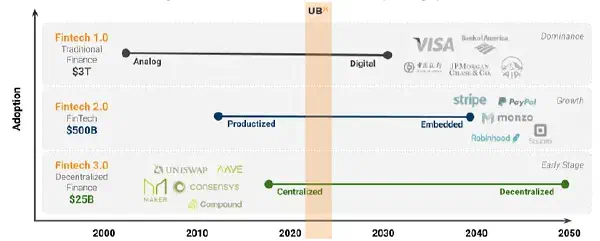

? What is the difference between Open Finance and Open Banking?

Open Banking is limited to bank account data. Open Finance expands that scope to include insurance, investments, and even utility data, creating a holistic view of the customer’s financial life.

? Why is Southeast Asia the next frontier for Embedded Finance?

Because of the high rate of “unbanked” or “underbanked” individuals who already use smartphones for commerce. Embedded finance allows us to reach these customers through the platforms they already trust.

? How does regulatory compliance become a competitive advantage?

When you are fully compliant and licensed, you gain trust—the most valuable currency in finance. It also allows you to partner with larger institutions and access cheaper capital, which is the ultimate fuel for scale.

Featured Insights on Fintech#