Last year, millions of dollars were wagered on whether Taylor Swift would appear at the Super Bowl or who the next Pope would be. To the casual observer, prediction markets look like a high-tech casino, a playground for “degens” and speculators.

But if you look under the hood, you’ll see something far more significant: The most efficient price-discovery engine for risk ever invented.

As we look toward the next decade of fintech, the real story isn’t about gambling. It’s about the convergence of prediction markets and parametric insurance. We are moving toward a world where “risk” is no longer a static contract tucked away in a filing cabinet, but a liquid, tradable commodity.

The Problem with Traditional Safety Nets#

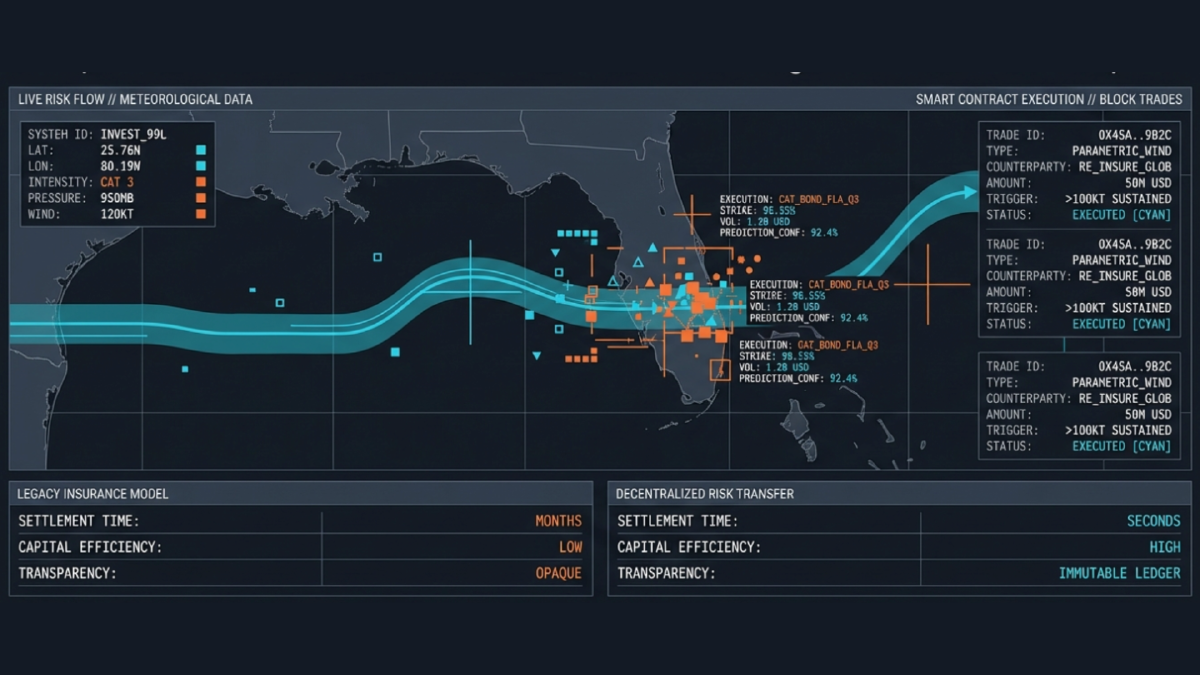

Historically, if a farmer wanted to protect their crop against drought, they had two choices: traditional indemnity insurance (which takes months to pay out and requires painful loss adjustments) or parametric insurance.

Parametric insurance was a massive leap forward. By triggering a payout based on a specific data point (say, less than 10cm of rainfall) it removed the subjectivity of claims. It’s fast, but it’s rigid. The premium is set by an underwriter’s model, often months in advance, and once you’re in, you’re locked in.

The Graduation to “Economic Good”#

Prediction markets take the “speed” of parametric insurance and add real-time liquidity.

When a farmer buys a “Drought” contract on a prediction market, they aren’t just “betting.” They are hedging. This shift from gambling to utility happens the moment these markets achieve enough depth to provide a reliable price signal.

How they differ in the real world:

- Parametric Insurance is a bespoke suit: made for you, but hard to change.

- Prediction Markets are a global wardrobe: you can buy, sell, or trade your “fit” as the weather (literally) changes.

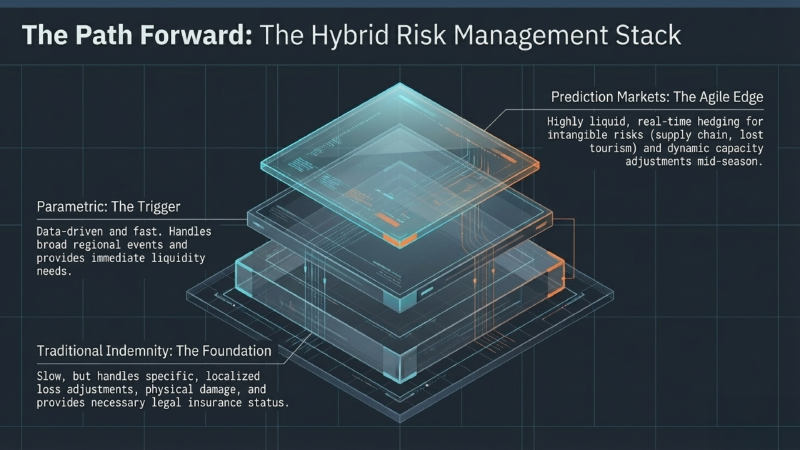

The Synergy: A New Layer of the Stack#

The most exciting part of this evolution isn’t “either/or”. It’s the interplay. We are entering an era of Synthetic Reinsurance.

Imagine a boutique insurance firm that offers parametric drought policies to coffee farmers in Ethiopia. If a sudden El Niño pattern emerges, that insurer is suddenly over-exposed. In the old world, they’d have to negotiate a complex reinsurance treaty.

In the new world, they go to a prediction market. By buying “Yes” contracts on the drought event they’ve insured against, they can hedge their own underwriting in real-time. The prediction market becomes the “insurance for the insurers.”

Why This Matters for the C-Suite#

We are witnessing the commoditization of uncertainty.

For fintech leaders, the opportunity isn’t just in building the platforms where people trade. It’s in building the middleware that connects these two worlds. It’s the oracles that feed the data, the regulatory wrappers that turn “bets” into “hedges,” and the liquidity pools that make it all possible.

Prediction markets aren’t graduating from the casino to the boardroom: they are becoming the floor of the boardroom itself.

The question is no longer if these markets are an economic good. The question is: are you liquid enough to survive the transition?

Read Next