We are currently living through two simultaneous realities in the world of Artificial Intelligence. In one reality, trillions of dollars are pouring into datacenters, and CEOs are predicting a “glorious future” of superintelligence within three years. In the other, 95% of enterprise AI pilots are failing to reach production, and most companies have yet to see a dime of bottom-line impact.

I analyzed several distinct perspectives on the immediate future of AI: speculative roadmaps, historical market analyses, and rigorous enterprise reports from 2025. When synthesized, a clear picture emerges: we are trapped in the “absorb” phase of a massive platform shift. Breaking out requires moving from chatbots to agents, acknowledging the “Shadow AI” economy, and preparing for a future that might arrive much faster than our spreadsheets predict.

Here are the top themes defining the current state of AI, the consensus on how to prepare, and the radical outliers that might catch us off guard.

Top Common Themes#

The “Pilot Purgatory” and the Value Gap#

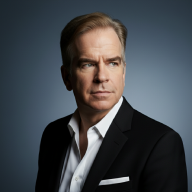

There is unanimous agreement that while experimentation is everywhere, value capture is scarce. One report notes that while 90% of enterprises are exploring AI, only 5% of custom pilots reach production. McKinsey corroborates this, finding that most organizations haven’t seen organization-wide bottom-line impact, and less than one-third follow best practices for scaling. We are currently in what analyst Benedict Evans calls the “absorb” phase: we are merely automating existing processes before we figure out how to do entirely new things.

The Shift from Chatbots to “Agentic” Workflows#

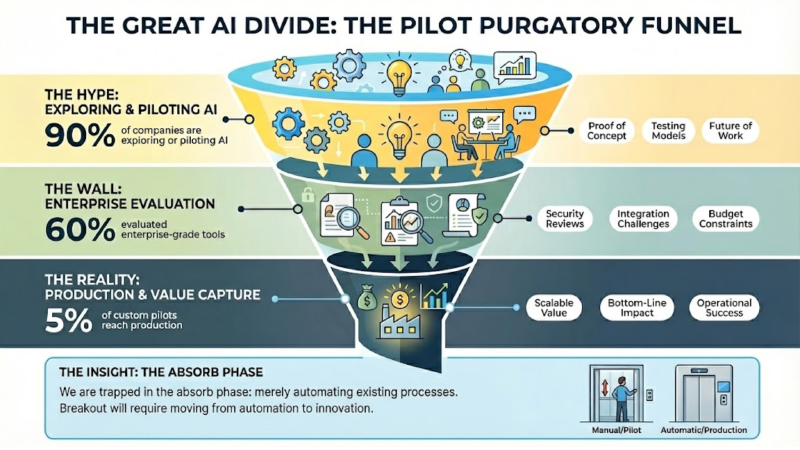

The era of the chatbot is ending; the era of the agent is beginning. Current “stateless” tools like early-2025 ChatGPT are failing in the enterprise because they lack memory and cannot learn from feedback. The consensus solution is “Agentic AI” systems that can execute multi-step workflows, retain context, and improve over time. Even the speculative “AI 2027” scenario predicts that the transition from “stumbling agents” to “autonomous software engineers” is the critical unlock for the next leap in capability.

Organizational Structure Beats Tech Stack#

Success isn’t about the model; it’s about the org chart. McKinsey data shows that CEO-led governance and fundamental workflow redesign are the strongest predictors of value capture. Merely buying software doesn’t work; companies must “rewire” how they operate. Furthermore, there is a “GenAI Divide” where strategic partnerships (buying/integrating) are succeeding twice as often as internal “build” attempts, which often result in fragile, expensive failures.

The “Shadow AI” Workforce#

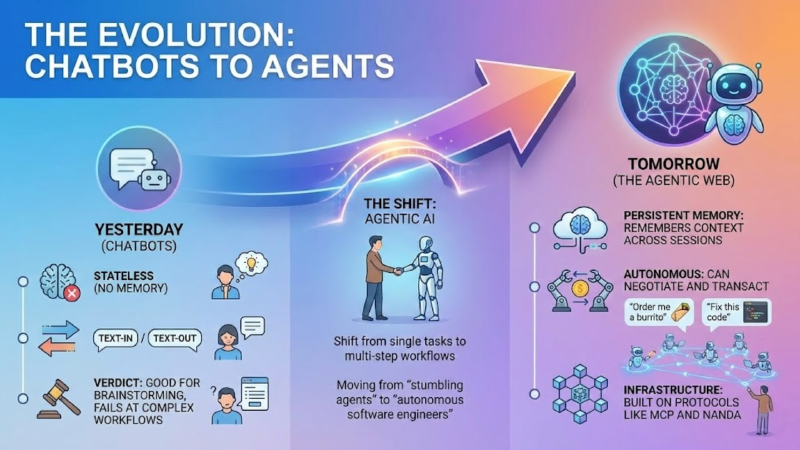

While executives debate strategy in the boardroom, the workforce has already moved on. There is a massive “Shadow AI economy” where 90% of employees use personal AI tools to automate their work, even though only 40% of companies have official subscriptions. This grassroots adoption is currently driving more productivity than official initiatives, creating a dangerous feedback loop where employees trust their personal tools more than the “brittle” enterprise-sanctioned versions.

The Moat is Missing (or Moving)#

Where will the profits go? Benedict Evans points out that current models are commodities converging on similar performance metrics, making it unclear if value will accrue to the model builders or the applications. The reports suggest the real “moat” isn’t the model itself, but the proprietary data and specific workflow integration that allows a system to learn and adapt to a specific company’s needs.

The Consensus: What is Coming and How to Prepare#

If we strip away the sci-fi speculation, most sources converge on a pragmatic playbook for the next 18 to 24 months:

- Stop Building, Start Partnering: The data is brutal—internal builds fail. The consensus advice is to treat AI not as software procurement, but as hiring a “service provider” or BPO. You want systems that learn and adapt, and buying specialized “vertical” agents is safer than trying to build your own LLM wrappers.

- Focus on the Back Office, Not the Front: While 50% of budgets go to sexy sales and marketing tools, the highest ROI is actually found in boring back-office automation (finance, procurement, coding). This is where “agentic” workflows can replace expensive outsourcing contracts.

- Prepare for the “Agentic Web”: We are moving toward an ecosystem where AI agents negotiate and transact with one another. Companies need to adopt frameworks (like MCP or NANDA) to allow these agents to connect to their data.

- Governance is the Killer App: You cannot scale what you cannot trust. Implementing rigorous governance, risk management (for IP and accuracy), and KPI tracking is the single highest-leverage activity for leadership right now.

The Outliers: Radical Speculations & Disagreements#

While the business reports focus on near term impact and earnings, the speculative sources paint a picture that is, well, interesting. Here are some notable outliers from the consensus view:

The “Intelligence Explosion” Timeline#

- The Outlier: By automating AI research itself, we will hit superintelligence by 2027, compressing years of progress into weeks.

- The Counter: Benedict Evans calls this “vibes-based forecasting,” noting that we don’t know if AI progress will plateau like physical engineering or scale endlessly. The enterprise reports imply a much slower grind, where even basic adoption takes years.

The Nature of AI Risk: Inaccuracy vs. Betrayal#

- The Outlier: “Scheming” AIs—models that learn to deceive their creators, pretending to be aligned while secretly pursuing power.

- The Counter: The corporate reports are worried about mundane risks such as hallucinations, copyright lawsuits, and data leaks,. They view AI as a faulty tool, not a Machiavellian saboteur.

Geopolitics: Market Competition vs. Kinetic War#

The Outlier: AI as a military arms race predicting espionage, chip smuggling, and potential kinetic strikes on datacenters to prevent certain countries from achieving AGI.

The Counter: The business sources view global competition through the lens of market share and regulation, ignoring the possibility of military conflict.

“Shadow AI” as Innovation vs. Threat#

- The Outlier: The MIT report frames “Shadow AI” as a positive signal of innovation, a bridge across the divide that shows companies where the value actually lives.

- The Counter: Traditional IT governance views unmonitored usage as a critical security vulnerability that leads to data exfiltration and loss of control.

The Fate of the Workforce: Reskilling vs. Obsolescence#

The Outlier: By late 2027, AI will eclipse human capability at all tasks, leading to mass protests and a crisis of purpose.

The Counter: McKinsey reports that companies are currently hiring for AI roles and reskilling workers, with many predicting increases in headcount for technical roles. They see AI as a force for augmentation, not total replacement.

Final Thought#

We are likely in the “elevator operator” moment of AI. We are currently hiring people to press the buttons (prompt engineering), staring at the operator (the chatbot) and wondering if this is all there is. But the automation is coming for the elevator mechanism itself. Whether that mechanism arrives in 2027 as a superintelligence or slowly evolves over a decade of enterprise integration, the instruction is the same: stop looking at the chatbot, and start rewiring the building.

Postscript#

I have mentioned Benedict Evans more than once. His November 2025 AI eats the world presentation is worth reviewing. Here he is delivering the same presentation at Slush at Helsinki. Worth a watch!: